Dot-com bubble

The "dot-com bubble" (or sometimes "IT bubble"[1] or "TMT bubble") was a speculative bubble covering roughly 1995–2000 (with a climax on March 10, 2000 with the NASDAQ peaking at 5132.52) during which stock markets in industrialized nations saw their equity value rise rapidly from growth in the more recent Internet sector and related fields. While the latter part was a boom and bust cycle, the Internet boom sometimes is meant to refer to the steady commercial growth of the Internet with the advent of the world wide web as exemplified by the first release of the Mosaic web browser in 1993 and continuing through the 1990s.

The period was marked by the founding (and, in many cases, spectacular failure) of a group of new Internet-based companies commonly referred to as dot-coms. Companies were seeing their stock prices shoot up if they simply added an "e-" prefix to their name and/or a ".com" to the end, which one author called "prefix investing".[2]

A combination of rapidly increasing stock prices, market confidence that the companies would turn future profits, individual speculation in stocks, and widely available venture capital created an environment in which many investors were willing to overlook traditional metrics such as P/E ratio in favor of confidence in technological advancements.

Contents |

Bubble growth

The venture capitalists saw record-setting rises in stock valuations of dot-com companies, and therefore moved faster and with less caution than usual, choosing to mitigate the risk by starting many contenders and letting the market decide which would succeed. The low interest rates in 1998–99 helped increase the start-up capital amounts. Although a number of these new entrepreneurs had realistic plans and administrative ability, many more of them lacked these characteristics but were able to sell their ideas to investors because of the novelty of the dot-com concept.

A canonical "dot-com" company's business model relied on harnessing network effects by operating at a sustained net loss to build market share (or mind share). These companies offered their services or end product for free with the expectation that they could build enough brand awareness to charge profitable rates for their services later. The motto "get big fast" reflected this strategy.[3] During the loss period the companies relied on venture capital and especially initial public offerings of stock to pay their expenses while having no source of income at all. The novelty of these stocks, combined with the difficulty of valuing the companies, sent many stocks to dizzying heights and made the initial controllers of the company wildly rich on paper.

Historically, the dot-com boom can be seen as similar to a number of other technology-inspired booms of the past including railroads in the 1840s, automobiles and radio in the 1920s and transistor electronics in the 1950s.

Soaring stocks

In financial markets, a stock market bubble is a self-perpetuating rise or boom in the share prices of stocks of a particular industry. The term may be used with certainty only in retrospect when share prices have since crashed. A bubble occurs when speculators note the fast increase in value and decide to buy in anticipation of further rises, rather than because the shares are undervalued. Typically many companies thus become grossly overvalued. When the bubble "bursts", the share prices fall dramatically, and many companies go out of business.

The dot-com model was inherently flawed: a vast number of companies all had the same business plan of monopolizing their respective sectors through network effects, and it was clear that even if the plan was sound, there could only be one network-effects winner in each sector, and therefore that most companies with this business plan would fail. In fact, many sectors could not support even one company powered entirely by network effects.

In spite of this, however, a few company founders made vast fortunes when their companies were bought out at an early stage in the dot-com stock market bubble. These early successes made the bubble even more buoyant. An unprecedented amount of personal investing occurred during the boom, and the press reported the phenomenon of people quitting their jobs to become full-time day traders.[4][5][6]

Free spending

According to dot-com theory, an Internet company's survival depended on expanding its customer base as rapidly as possible, even if it produced large annual losses. For instance, Google and Amazon did not see any profit in their first years. Amazon was spending on expanding customer base and letting people know that it existed and Google was busy spending on creating more powerful machine capacity to serve its expanding search engine. The phrase "Get large or get lost" was the wisdom of the day.[7] At the height of the boom, it was possible for a promising dot-com to make an initial public offering (IPO) of its stock and raise a substantial amount of money even though it had never made a profit — or, in some cases, earned any revenue what so ever. In such a situation, a company's lifespan was measured by its burn rate: that is, the rate at which a non-profitable company lacking a viable business model ran through its capital served as the metric.

Public awareness campaigns were one of the ways in which dot-coms sought to grow their customer base. These included television ads, print ads, and targeting of professional sporting events. Many dot-coms named themselves with onomatopoeic nonsense words that they hoped would be memorable and not easily confused with a competitor. Super Bowl XXXIV in January 2000 featured seventeen dot-com companies that each paid over two million dollars for a thirty-second spot. By contrast, in January 2001, just three dot-coms bought advertising spots during Super Bowl XXXV. In a similar vein, CBS-backed iWon.com gave away ten million dollars to a lucky contestant on an April 15, 2000, on a half-hour primetime special that was broadcast on CBS.

Not surprisingly, the "growth over profits" mentality and the aura of "new economy" invincibility led some companies to engage in lavish internal spending, such as elaborate business facilities and luxury vacations for employees. Executives and employees who were paid with stock options instead of cash became instant millionaires when the company made its initial public offering; many invested their new wealth into yet more dot-coms.

Cities all over the United States sought to become the "next Silicon Valley" by building network-enabled office space to attract Internet entrepreneurs. Communication providers, convinced that the future economy would require ubiquitous broadband access, went deeply into debt to improve their networks with high-speed equipment and fiber optic cables. Companies that produced network equipment like Nortel Networks were irrevocably damaged by such over-extension; Nortel declared bankruptcy in early 2009. Companies like Cisco, which did not have any production facilities, but bought from other manufacturers, were able to leave quickly and actually do well from the situation as the bubble burst and products were sold cheaply.

Similarly, in Europe the vast amounts of cash the mobile operators spent on 3G licences in Germany, Italy, and the United Kingdom, for example, led them into deep debt. The investments were far out of proportion to both their current and projected cash flow, but this was not publicly acknowledged until as late as 2001 and 2002. Due to the highly networked nature of the IT industry, this quickly led to problems for small companies dependent on contracts from operators.

The bubble bursts

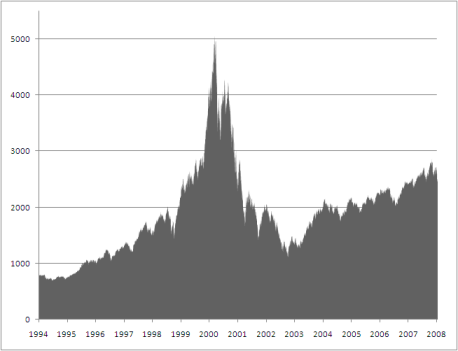

Over 1999 and early 2000, the U.S. Federal Reserve increased interest rates six times,[8] and the economy began to lose speed. The dot-com bubble burst, numerically, on March 10, 2000, when the technology heavy NASDAQ Composite index[9], peaked at 5,048.62 (intra-day peak 5,132.52), more than double its value just a year before. The NASDAQ fell slightly after that, but this was attributed to correction by most market analysts; the actual reversal and subsequent bear market may have been triggered by the adverse findings of fact in the United States v. Microsoft case which was being heard in federal court. The findings, which declared Microsoft a monopoly, were widely expected in the weeks before their release on April 3.

One possible cause for the collapse of the NASDAQ (and all dotcoms that collapsed) was the massive, multi-billion dollar sell orders for major bellwether high tech stocks (Cisco, IBM, Dell, etc.) that happened by chance to be processed simultaneously on the Monday morning following the March 10 weekend. This selling resulted in the NASDAQ opening roughly four percentage points lower on Monday March 13 from 5,038 to 4,879—the greatest percentage 'pre-market' selloff for the entire year.

The massive initial batch of sell orders processed on Monday, March 13 triggered a chain reaction of selling that fed on itself as investors, funds, and institutions liquidated positions. In just six days the NASDAQ had lost nearly nine percent, falling from roughly 5,050 on March 10 to 4,580 on March 15.

Another reason may have been accelerated business spending in preparation for the Y2K switchover. Once New Year had passed without incident, businesses found themselves with all the equipment they needed for some time, and business spending quickly declined. This correlates quite closely to the peak of U.S. stock markets. The Dow Jones peaked on January 14, 2000 (closed at 11,722.98)[10] and the broader S&P 500 on March 24, 2000 (closed at 1,527.46);[11] while, even more dramatically the UK's FTSE 100 Index peaked at 6,950.60 on the last day of trading in 1999 (December 30). Hiring freezes, layoffs, and consolidations followed in several industries, especially in the dot-com sector.

The bursting of the bubble may also have been related to the poor results of Internet retailers following the 1999 Christmas season. This was the first unequivocal and public evidence that the "Get Rich Quick" Internet strategy was flawed for most companies. These retailers' results were made public in March when annual and quarterly reports of public firms were released.

Some of the big business houses totally ignored the fundamentals and presumed that in the name of internet or new economy anything can be sold online and one can become a market leader overnight. One of the classic examples of this approach was that companies attempted to use a cookie cutter model as they tried to spread their wings on the global map. Many companies simply ignored the basic rules of due diligence of potential target market and customer base with respect to local market and needs. If an idea was successful in USA, it was assumed to be successful in other parts of the world, which turned out to be incorrect.

By 2001 the bubble was deflating at full speed. A majority of the dot-coms ceased trading after burning through their venture capital, many having never made a net profit. Investors often referred to these failed dot-coms as "dot-bombs".

Aftermath

On January 11, 2000, America Online, a favorite of dot-com investors and pioneer of dial-up Internet access, acquired Time Warner, the world's largest media company.[12] The transaction has been described as "the worst in history".[13] Within two years, boardroom disagreements drove out both of the CEOs who made the deal, and in October 2003 AOL Time Warner dropped "AOL" from its name.

Several communication companies could not weather the financial burden and were forced to file for bankruptcy. One of the more significant players, WorldCom, was found practicing illegal accounting practices to exaggerate its profits on a yearly basis. WorldCom's stock price fell drastically when this information went public and eventually filed the third largest corporate bankruptcy in U.S. history Other examples include NorthPoint Communications, Global Crossing, JDS Uniphase, XO Communications, and Covad Communications. Companies such as Nortel, Cisco and Corning, were at a disadvantage because they relied on infrastructure that was never developed which caused the stock of Corning to drop significantly.

Many dot-coms ran out of capital and were acquired or liquidated; the domain names were picked up by old-economy competitors or domain name investors. Several companies and their executives were accused or convicted of fraud for misusing shareholders' money, and the U.S. Securities and Exchange Commission fined top investment firms like Citigroup and Merrill Lynch millions of dollars for misleading investors. Various supporting industries, such as advertising and shipping, scaled back their operations as demand for their services fell. A few large dot-com companies, such as Amazon.com and eBay, survived the turmoil and appear assured of long-term survival, while others such as Google have become industry-dominating mega-firms.

The Stock Market Crash of 2000-2002 caused the loss of $5 trillion in the market value of companies from March 2000 to October 2002.[14] The terrorist destruction of the World Trade Center on September 11, 2001, with the loss of about 650 Cantor Fitzgerald LP investment employees alone, required the NYSE's trading to be halted for four sessions while new trading sites were being established.

More in-depth analysis shows that 50% of the dot-coms companies survived through 2004. With this, it is safe to assume that the assets lost from the Stock Market does not directly link to the closing of firms. More importantly, however, it can be concluded that even companies who were categorized as the "small players" were adequate enough to endure the destruction of the financial market during 2000-2002.[15]

One good byproduct that came out of this crash was a fresh realization of a new channel to the old economy companies. Many of these companies stayed true to their core business fundamental values but expanded their reach and potential by rightly balancing and utilizing the new e-channel, whether it was a B2B (Business to Business) or B2C (Business to Customer) approach to the business.

Nevertheless, laid-off technology experts, such as computer programmers, found a glutted job market. In the U.S., International outsourcing and the recently allowed increase of skilled visa "guest workers" (e.g., those participating in the U.S. H-1B visa program) exacerbated the situation.[16] University degree programs for computer-related careers saw a noticeable drop in new students. Anecdotes of unemployed programmers going back to school to become accountants or lawyers were common.

The transition of the bubbles

Some believe the crash of the dot-com bubble mutated to the housing bubble in the U.S.

Yale economist Robert Shiller said in 2005, “Once stocks fell, real estate became the primary outlet for the speculative frenzy that the stock market had unleashed. Where else could plungers apply their newly acquired trading talents? The materialistic display of the big house also has become a salve to bruised egos of disappointed stock investors. These days, the only thing that comes close to real estate as a national obsession is poker.”[17]

Ralph Block wrote in 2005: "Many baby boomers appear to have decided that the stock market won’t provide them with sufficient assets with which to retire, and have taken advantage of “hot” real estate markets and low (e.g., 5 percent) down payments to speculate in residential real estate. The number of homes bought for investment jumped 50 percent during the four year period ending in 2004, according to the San Francisco research firm LoanPerformance."[18]

However, the housing bubble transformed into the current full scale subprime mortgage crisis which started in late 2007.

List of companies significant to the bubble

For discussion and a list of dot-com companies outside the scope of the dot-com bubble, see dot-com company.

- Boo.com, spent $188 million in just six months[19] in an attempt to create a global online fashion store. Went bankrupt in May 2000.[20]

- Startups.com was the "ultimate dot-com startup". Went out of business in 2002.

- e.Digital Corporation (EDIG): Long term unprofitable OTCBB traded company founded in 1988 previously named Norris Communications. Changed its name to e.Digital in January 1999 when stock was at $0.06 level. The stock rose rapidly in 1999 and went from closing price of $2.91 on December 31, 1999 to intraday high of $24.50 on January 24, 2000. It quickly retraced and has traded between $0.08 and $0.20 in 2008 and 2009.[21]

- Freeinternet.com – Filed for bankruptcy in October 2000, soon after canceling its IPO. At the time Freeinternet.com was the fifth largest ISP in the United States, with 3.2 million users.[22] Famous for its mascot Baby Bob, the company lost $19 million in 1999 on revenues of less than $1 million.[23][24]

- GeoCities, purchased by Yahoo! for $3.57 billion in January 1999. Yahoo! closed GeoCities on October 26, 2009.[25]

- theGlobe.com – Was a social networking service, that went live in April 1995 and made headlines by going public on November 1998 and posting the largest first day gain of any IPO in history up to that date. The CEO became in 1999 a visible symbol of the excesses of dot-com millionaires.

- GovWorks.com – the doomed dot-com featured in the documentary film Startup.com.

- Hotmail – founder Sabeer Bhatia sold the company to Microsoft for $400 million;[26] at that time Hotmail had 9 million members.[27]

- InfoSpace – In March 2000 this stock reached a price $1,305 per share,[28] but by April 2001 its price had crashed down to $22 a share.[28]

- lastminute.com, whose IPO in the U.K. coincided with the bursting of the bubble.

- The Learning Company, bought by Mattel in 1999 for $3.5 billion, sold for $27.3 million in 2000.[29]

- Think Tools AG, one of the most extreme symptoms of the bubble in Europe: market valuation of CHF 2.5 billion in March 2000, no prospects of having a substantial product (investor deception), followed by a collapse.[30]

- Xcelera.com, a Swedish investor in start-up technology firms.[31] "greatest one-year rise of any exchange-listed stock in the history of Wall Street." [32]

See also

Terminology

- Bankruptcy

- Digital Revolution

- E-commerce

- Irrational exuberance

- The Long Tail

- The South Sea Company

- Stock market boom

- Stock market bubble

- Tulip mania

- Techno-utopianism

- Technology hype

- Web 2.0

- E-learning

- Dark Fiber

Media

- e-Dreams

- SatireWire

- Startup.com

- ebay.com

Venture capital

- List of venture capital firms

Economic downturn

- Financial crisis of 2007-2010

- Subprime mortgage crisis

- United States housing bubble

Also see

- Oil price increases since 2003

- 2007–2008 world food price crisis

- 2000s commodities boom

- Worldcom

Further reading

- Cassidy, John. Dot.con: How America Lost its Mind and Its Money in the Internet Era (2002)

- Daisey, Mike. 21 Dog Years Free Press. ISBN 0-7432-2580-5.

- Goldfarb, Brent D., Kirsch, David and Miller, David A., "Was There Too Little Entry During the Dot Com Era?" (April 24, 2006). Robert H. Smith School Research Paper No. RHS 06-029 Available at SSRN: http://ssrn.com/abstract=899100

- Kindleberger, Charles P., Manias, Panics, and Crashes: A History of Financial Crises (Wiley, 2005, 5th edition)

- Kuo, David dot.bomb: My Days and Nights at an Internet Goliath ISBN 0-316-60005-9 (2001)

- Lowenstein, Roger. Origins of the Crash: The Great Bubble and Its Undoing. (Penguin Books, 2004) ISBN 0-14-303467-7

- Wolff, Michael. Burn Rate: How I Survived the Gold Rush Years on the Internet

References

- ↑ James K. Galbraith and Travis Hale (2004). Income Distribution and the Information Technology Bubble. University of Texas Inequality Project Working Paper

- ↑ Nanotech Excitement Boosts Wrong Stock, The Market by Mike Maznick, Techdirt.com, Dec 4, 2003

- ↑ Spector, Robert (2000). amazon.com: Get Big Fast. New York: HarperBusiness. ISBN 0066620414.

- ↑ Kadlec, Daniel (1999-08-09). "Day Trading: It's a Brutal World". Time. http://www.time.com/time/magazine/article/0,9171,991726,00.html. Retrieved 2007-10-09.

- ↑ Johns, Ray (1999-03-04). "Daytrader Trend". Online Newshour: Forum. PBS. http://www.pbs.org/newshour/forum/february99/daytraders.html. Retrieved 2007-10-09.

- ↑ Cringely, Robert X. (1999-12-16). "There's a Sucker Born Every 60,000 Milliseconds". I, Cringely. PBS. http://www.pbs.org/cringely/pulpit/1999/pulpit_19991216_000634.html. Retrieved 2007-10-09.

- ↑ How to Start a Startup

- ↑ "FRB: Monetary Policy, Open Market Operations". http://www.federalreserve.gov/fomc/fundsrate.htm. Retrieved 2009-07-01.

- ↑ Index Chart

- ↑ ^DJI: Historical Prices for DOW JONES INDUSTRIAL AVERAGE IN – Yahoo! Finance

- ↑ ^GSPC: Historical Prices for S&P 500 INDEX,RTH – Yahoo! Finance

- ↑ "Top Mergers & Acquisitions (M&A) Deals". 2007-03-28. http://www.manda-institute.org/en/statistics-top-m&a-deals-transactions.htm. Retrieved 2007-05-05.

- ↑ Time Warner, without Aol, tops forecasts on money.cnn.com

- ↑ Fears of Dot-Com Crash, Version 2.0

- ↑ Goldfarb, Brent D., Kirsch, David and Miller, David A., "Was There Too Little Entry During the Dot Com Era?" (April 24, 2006). Robert H. Smith School Research Paper No. RHS 06-029 Available at SSRN: http://ssrn.com/abstract=871210

- ↑ [1] "Indian Companies Abusing U.S. H-1B, L-1 Laws: A Study Ruining American Economy & Society – Dampening Recovery. SAN FRANCISCO: Jan 23, 2004 (PNS) – According to a research by Professor Ron Hira of Rochester Institute of Technology, India companies are abusing the temporary work visas by making a heave [sic] use of H-1B and L-1. The Indian companies have come under scrutiny their abuse practices which have accelerated shift of tech work to India causing anxiety and resentment among American work force."

- ↑ Jonathan R. Laing (2005-06-20). "The Bubble's New Home". Barron's Magazine. http://online.barrons.com/article/SB111905372884363176.html.

- ↑ Block, Ralph (January 1, 2006). Investing in REITs: Real Estate Investment Trusts. Bloomberg Press. p. 268. ISBN 1-57660-193-5.

- ↑ "INTERNATIONAL BUSINESS; Fashionmall.com Swoops In for the Boo.com Fire Sale". The New York Times. June 2, 2000. http://query.nytimes.com/gst/fullpage.html?res=9F05E4DB103CF931A35755C0A9669C8B63. Retrieved May 1, 2010.

- ↑ Top 10 dot-com flops – CNET.com

- ↑ Historical prices of EDIG stock

- ↑ Another One Bites the Dust – FreeInternet.com Files for Bankruptcy – Addlebrain.com

- ↑ InternetNews Realtime IT News – Freeinternet.com Scores User Surge

- ↑ ISP-Planet – News – Freei Files for Bankruptcy

- ↑ [2]

- ↑ BW Online | September 14, 2000 | Hotmail's Creator Is Starting Up Again, and Again, and

- ↑ Microsoft buys Hotmail – CNET News.com

- ↑ 28.0 28.1 http://seattletimes.nwsource.com/art/news/business/infospace/infospaceTimelineDay1_2_intro.swf

- ↑ Abigail Goldman (2002-12-06). "Mattel Settles Shareholders Lawsuit For $122 Million". Los Angeles Times. http://securities.stanford.edu/news-archive/2002/20021206_Settlement05_Goldman.htm.

- ↑ Don't Think Twice: Think Tools is Overvalued, The Wall Street Journal Europe, October 30, 2000

- ↑ Xcelera's FAQ's

- ↑ http://www.georgenichols.com/publishedwritings/xla/index.htm

External links

- Top 10 dot-com flops – CNet's list of ten most notable failed dot-com companies

- Startup Dot Com Movie – documentary of a failing company.

- Warren Buffett: 'I told you so' – BBC article, 13 March 2001.

|

|||||